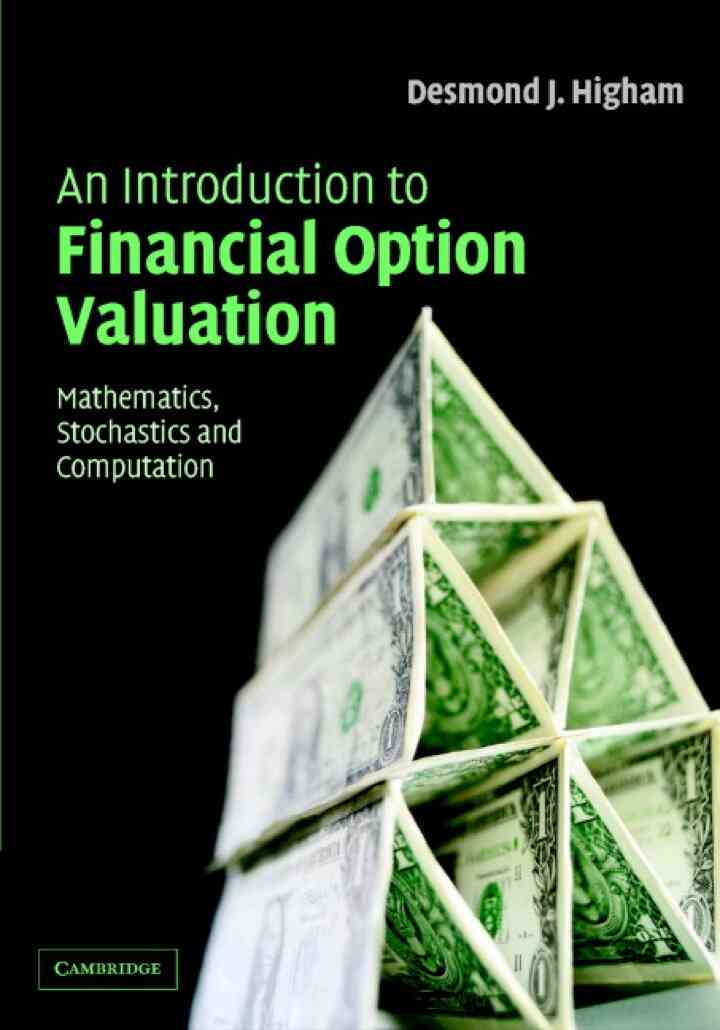

An Introduction to Financial Option Valuation: Mathematics, Stochastics and Computation

In stock$27.00

Format*

1

SKU:GC-5221221852

Comes to you in 7-11 business days under normal conditions.

Eligible for return within 30 days from delivery.

An Introduction to Financial Option Valuation: Mathematics, Stochastics and Computation

$27.00

This is a lively textbook providing a solid introduction to financial option valuation for undergraduate students armed with a working knowledge of a first year calculus.\n\nWritten in a series of short chapters, its self-contained treatment gives equal weight to applied mathematics, stochastics and computational algorithms. No prior background in probability, statistics or numerical analysis is required. Detailed derivations of both the basic asset price model and the Black�Scholes equation are provided along with a presentation of appropriate computational techniques including binomial, finite differences and in particular, variance reduction techniques for the Monte Carlo method. Each chapter comes complete with accompanying stand-alone MATLAB code listing to illustrate a key idea. Furthermore, the author has made heavy use of figures and examples, and has included computations based on real stock market data.An Introduction to Financial Option Valuation: Mathematics, Stochastics and Computation is written by Desmond J. Higham and published by Cambridge University Press. ISBNs for An Introduction to Financial Option Valuation are 9780511252785, 0511252781 and the print ISBNs are 9780521547574, 0521547571.

Product Details

TypeNew Arrivals

SKUGC-5221221852

TagsNew Arrivals

You May Also Like

View all →

Sustained Simulation Performance 2019 and 2020 Proceedings of the Joint Workshop on Sustained Simulation Performance, University of Stuttgart (HLRS) and Tohoku University, 2019: and 2020

$30.00

Handbook of Research on the Educator Continuum and Development of Teachers

$157.00

Handbook of Research on Advancing Equity and Inclusion Through Educational Technology

$184.00

Type 1 Diabetes, An Issue of Endocrinology and Metabolism Clinics of North America

$61.00